Your data stays yours

We never sell, share, or use your financial data for advertising. Your information is only ever used to power your own insights.

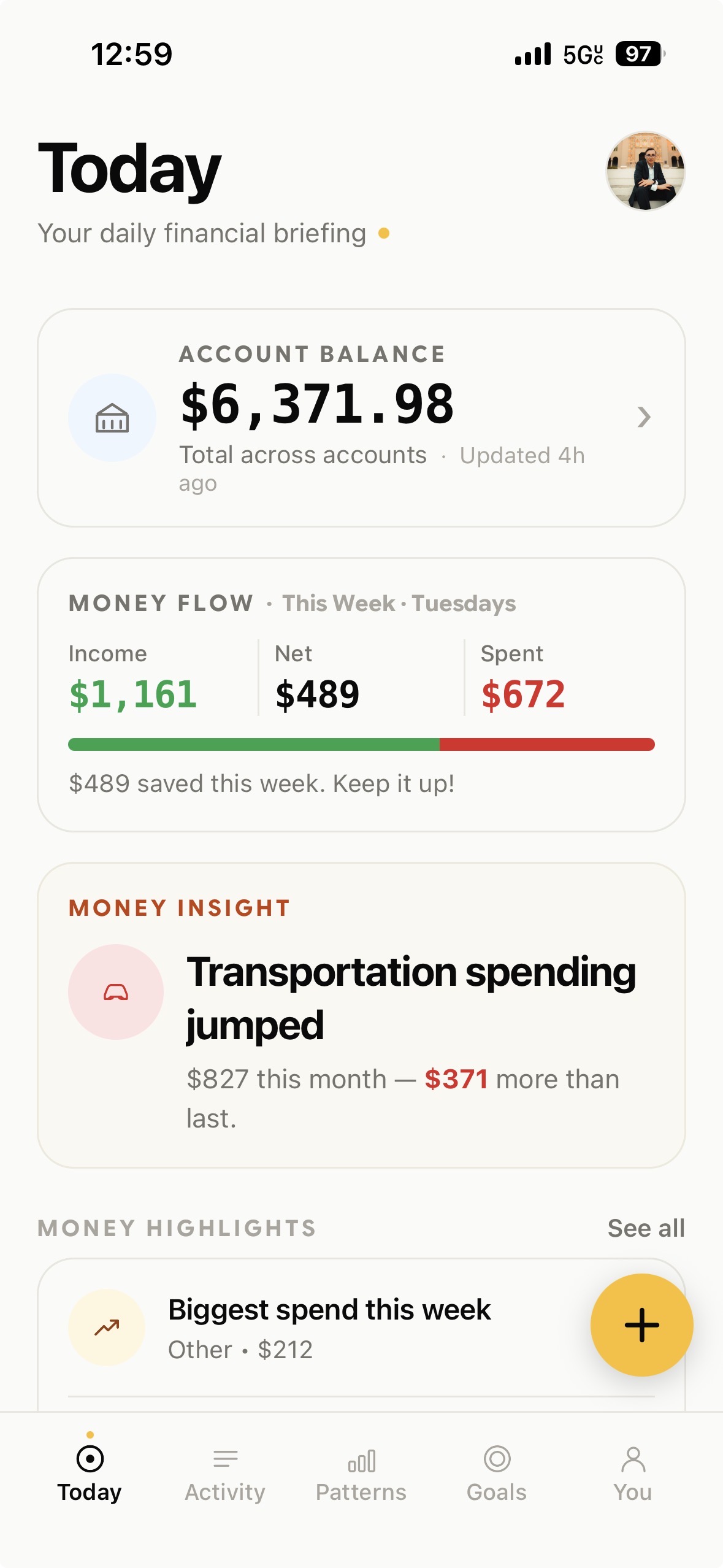

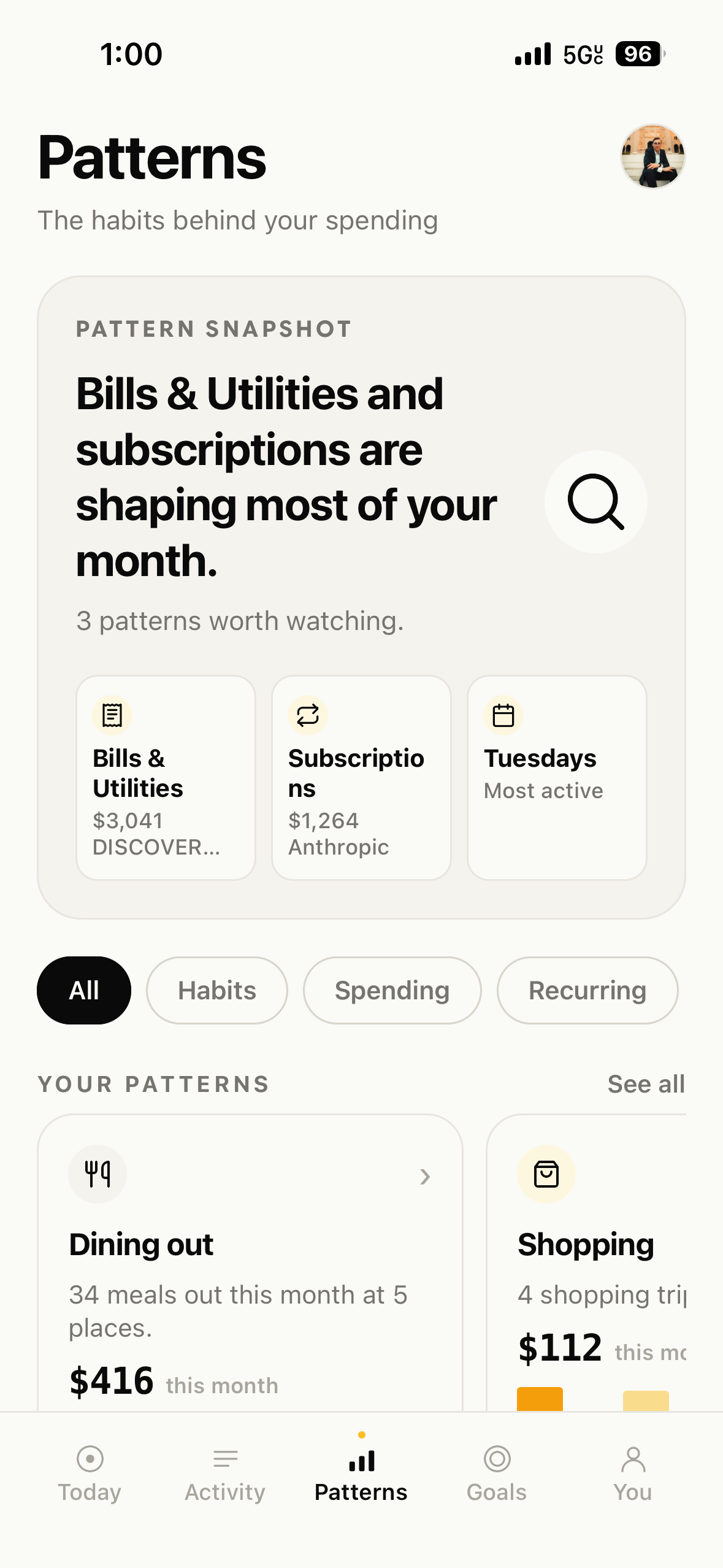

Finbird quietly watches your spending, catches small habits early, and tells you what to do about them — in plain language. No spreadsheets.

Free to download · 7-day Premium trial · No credit card required

Start your free 7-day Premium trial and connect your bank with Plaid in 2 minutes — or skip it and add transactions manually for free. No credit card required.

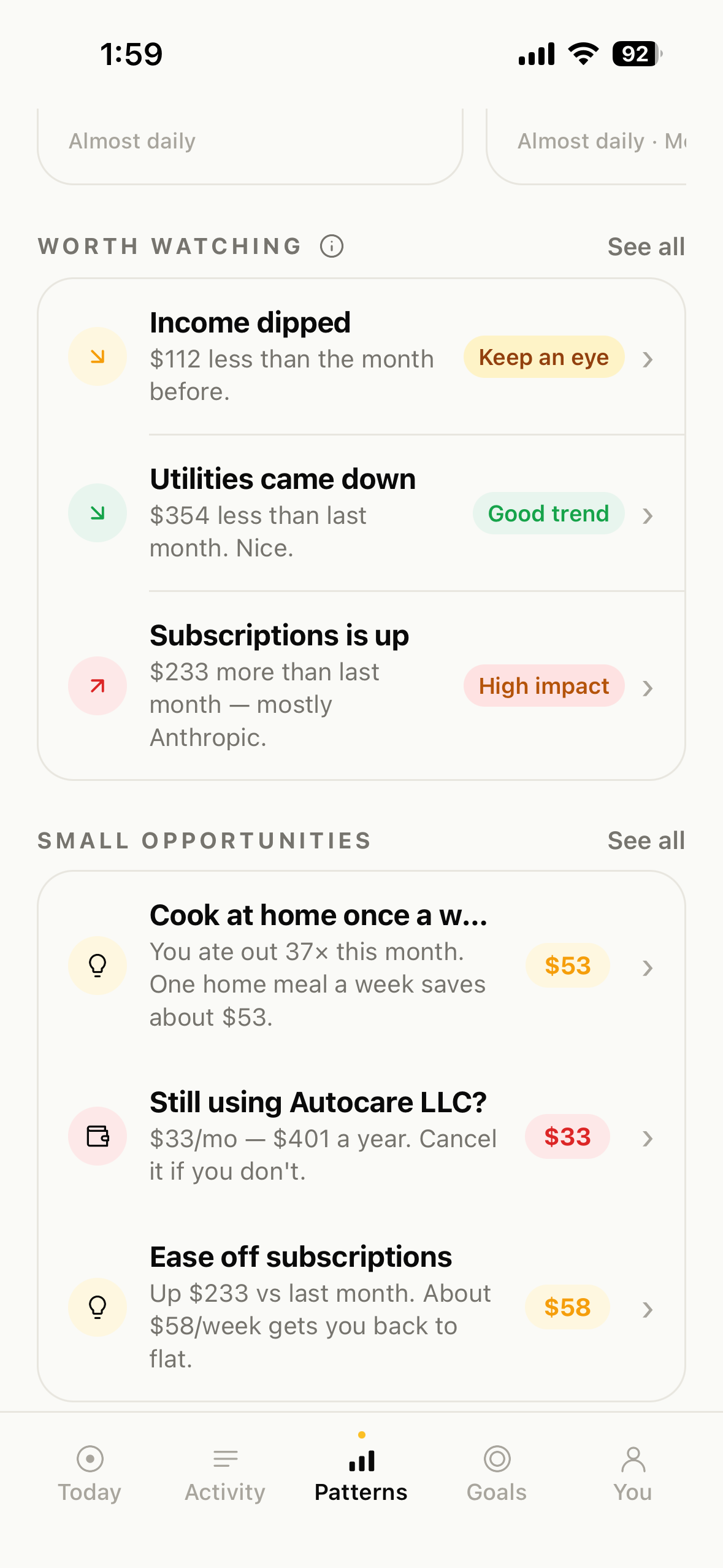

In the background, Finbird compares your spending to your own baseline and flags what's quietly changing.

Dining out is up $92 — mostly weekends after 7PM.

Each morning you open the app to a plain-language summary of what shifted — and why it actually matters.

Finbird suggests one realistic next step to stay on track. Small shifts, repeated — that's how the big future gets built.

We never sell, share, or use your financial data for advertising. Your information is only ever used to power your own insights.

All data is encrypted at rest and in transit using 256-bit AES encryption — the same standard used by major banks.

Bank connections use Plaid, a trusted financial data network. Finbird never sees or stores your bank login credentials.

When you connect your bank, Finbird has read-only access. We can see transactions — we cannot move money, ever.

One clear view. Nothing to decode.

Most finance apps bury you in charts and numbers. Finbird keeps things clear so you can understand your money faster.

Dining out

12 visits this month

A habit you might not notice.

See spending habits you may miss. Understand where your money goes and why.

Cook at home once a week.

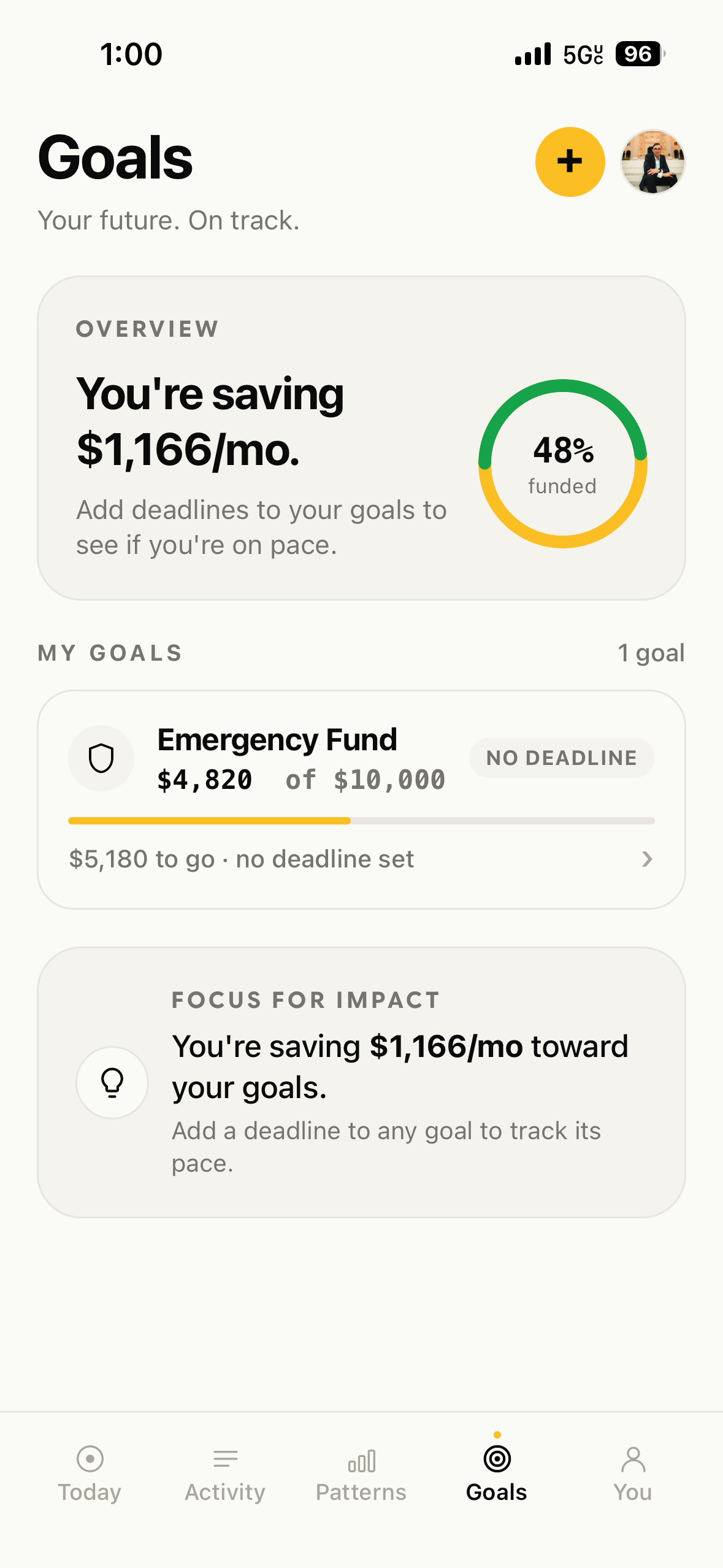

Every insight has a purpose. Spend smarter, save more, and stay on track.

Finbird is free to download. You get a 7-day Premium trial when you sign up so you can connect your bank and try automatic syncing. After the trial, you can keep using Finbird free with manual transaction tracking — or stay on Premium for automatic bank sync and the full insight engine.

No. Connecting your bank is optional and only unlocks automatic syncing during the trial and on Premium. If you'd rather keep things manual, you can use Finbird free forever without ever linking an account.

Nothing surprising. If you don't subscribe, your bank connection switches off and the app drops to the free manual tier — your data, history, and goals all stay. You won't be charged unless you choose to keep Premium, and there's no credit card required to start the trial.

Yes. We use bank-level 256-bit encryption and connect through Plaid, so Finbird never sees or stores your bank login. Connections are read-only — we can see transactions but can never move money.

Banking apps show you raw data and leave you to interpret it. Finbird reads the patterns for you, tells you what changed in plain language, and suggests one realistic next step.

Finbird is available on iPhone and iPad, with iCloud sync so your insights stay current across every Apple device you sign in on.

Absolutely. Premium is month-to-month or yearly and you can cancel in a couple of taps inside Settings → Apple ID → Subscriptions. Your data is always yours and you can export it whenever you like.

Download Finbird free and see what your money has been trying to tell you.

Free to download · 7-day Premium trial · No credit card required